A. Sample completed Form 1094-B

Thank you for accessing Kinney Health Compliance.

You must own a Affordable Care Act Membership Plan to continue reading.

B. Sample Completed form 1095-B (Full-Text)

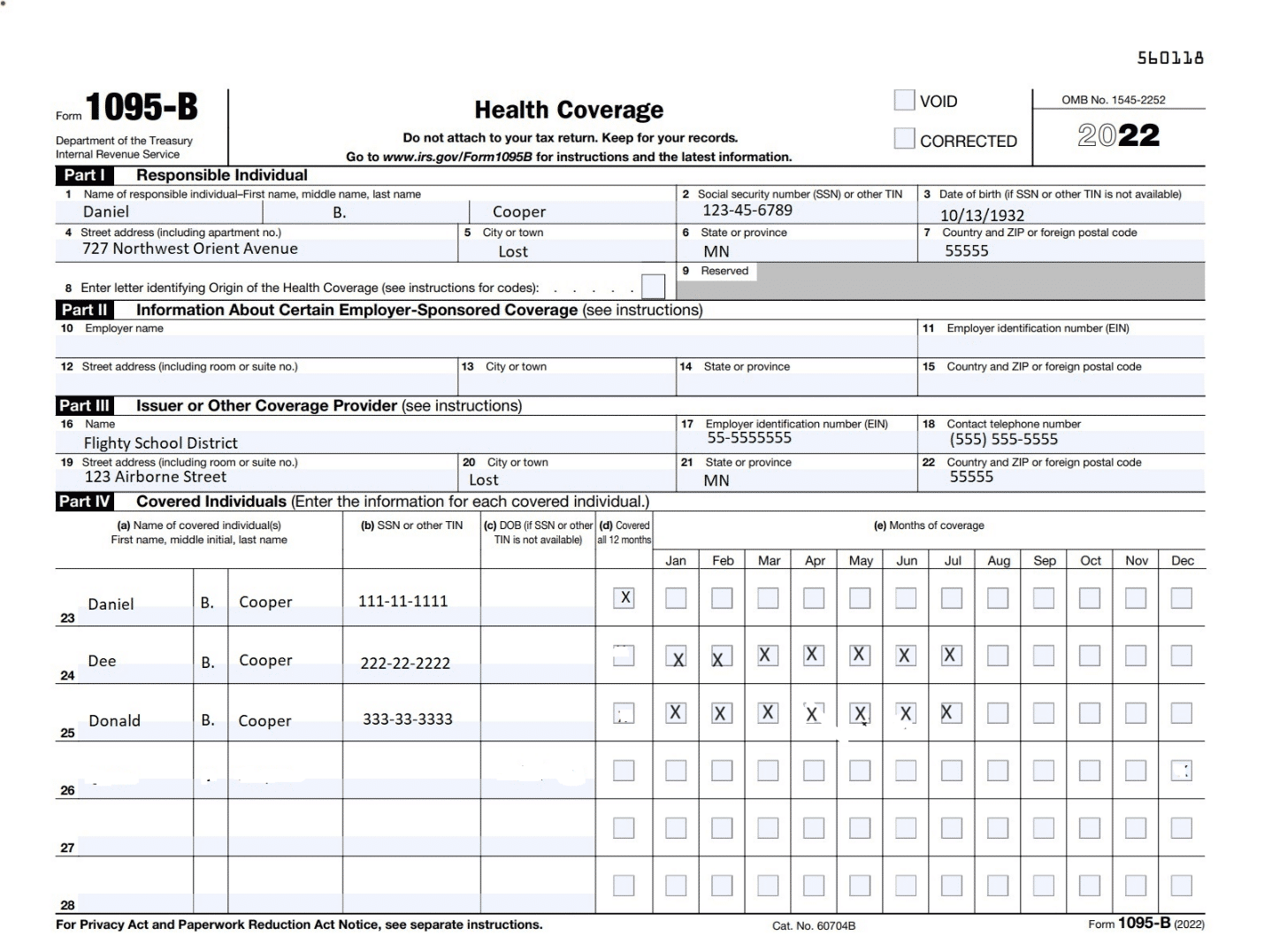

B-1. The untold story of D.B. Cooper. Many of you know the story of D.B. Cooper, who famously hijacked a jet in 1971 and parachuted into the wilderness with $200,000 in cash. What most don’t know is that he reappeared in Lost, Minnesota many years later and became a principal with the Flighty School District. By that time he was 85 years old, had sewn his wild oats, and it was time to settle down and start a family. He married a stewardess, Dee, and they had two children. Darla B. Cooper was born in December of 2022, when D.B. Cooper was 90 years old.[1]

Let’s take a look at Form 1095-B for D.B. Cooper. What follows is the version to be sent to the IRS in 2023 for calendar year 2022. The version furnished to D.B. (Daniel B.) Cooper will have truncated social security numbers).

- Part I

- Part II

Is left blank. Part II is only completed by insurance companies for fully insured health plans. If you are a small employer with a fully insured plan, most insurance companies will complete Forms 1094-B and 1095-B, furnish Form 1095-B to individuals, and file both forms with the IRS (but confirm before assuming). [Note: Applicable large employers are responsible for completing, filing, and furnishing Forms 1094-C and 1095-C, even if they have fully insurance health plans]. Lost, Minnesota is a small employer, but it has a self-insured group health plan, so it is responsible for preparing, filing and furnishing Form 1094-B and 1095-C. The preparer should leave Part II blank.

- Part III

Complete the name, address, EIN, and phone number of the employer plan sponsor.

- Part IV

D.B. Cooper is listed first, followed by all members of his family who are covered by the plan. D.B. Cooper, Dee, and Donald were covered all 12 months of 2022, and the “all 12 months” box is checked in Part IV, paragraph (d). Darla was born on December 1 and has coverage from that date forward, which is why the December box is checked for her. She has not yet received her SSN, so the employer uses her date of birth.

B-2. D.B. Cooper gets divorced. Now let’s suppose that, in early 2022, Dee discovers that Dan is planning another airline hijacking. She is fed up with Dan and his shenanigans, and files for divorce. The divorce is finalized on July 15th, 2022, and custody of the children to go Dee. Dee and the kids have coverage through the end of July, and she elects family continuation coverage under both COBRA and state continuation coverage.[2] The Form 1095-B sent to the IRS in 2023 will look like this (the version furnished to Dan will include truncated social security numbers):

You’ll note that the baby, Darla B. Cooper, is missing from this form. This is because she has not been born yet by the time Dee and Donald lose coverage and elect COBRA effective August 1st.

Beginning in August, Dee B. Cooper is the “responsible person” with respect to the health plan for herself and her children. In 2023, Dee will receive her own Form 1095-B. It will look like this:

See how easy and fun this is?

[1] Wait, you ask, if he’s 90, why isn’t he on Medicare? He’s still actively employed, we answer, he doesn’t have to elect Medicare and if he does, it will on only pay claims that are (1) covered by Medicare and (2) not covered by the plan (i.e., it pays “secondary” when the Medicare recipient is actively employed). He can enroll without penalties later when he finally retires. But Medicare Part A is free, you ask. Why wouldn’t he at least enroll in Medicare Part A? Because D.B. Cooper wants to keep contributing to his HSA, we answer. He can’t do that if he enrolls in Medicare because the deductible is too low. Quit changing the subject!

[2] Why both? Because Minnesota public employees and their dependents should always elect both COBRA and state continuation coverage. Each has their pros and cons, but together, the coverage is more comprehensive. Under COBRA, coverage in the event of divorce is for up to 36 months. Under Minn. Stat. Sec. 62A.21, one of several state continuation coverage statutes, coverage in the event of divorce is indefinite (unless and until the spouse obtains other coverage or the children are no longer dependents). Selecting both forms of continuation coverage is like lining up two pieces of Swiss cheese so that their holes do not match.[/mepr-active]

B-1. The untold story of D.B. Cooper

Many of you know the story of D.B. Cooper, who famously hijacked a jet in 1971 and parachuted into the wilderness with $200,000 in cash. What most don’t know is that he reappeared in Lost, Minnesota many years later and became a principal with the Flighty School District. By that time he was 85 years old, had sewn his wild oats, and it was time to settle down and start a family. He married a stewardess, Dee, and they had two children. Darla B. Cooper was born in December of 2022, when D.B. Cooper was 90 years old.[1]

Let’s take a look at Form 1095-B for D.B. Cooper. What follows is the version to be sent to the IRS in 2023 for calendar year 2022. The version furnished to D.B. (Daniel B.) Cooper will have truncated social security numbers).

- Part I

Thank you for accessing Kinney Health Compliance.

You must own a Affordable Care Act Membership Plan to continue reading.

B-2. D.B. Cooper gets divorced

Now let’s suppose that, in early 2022, Dee discovers that Dan is planning another airline hijacking. She is fed up with Dan and his shenanigans, and files for divorce. The divorce is finalized on July 15th, 2022, and custody of the children to go Dee. Dee and the kids have coverage through the end of July, and she elects family continuation coverage under both COBRA and state continuation coverage.[1] The Form 1095-B sent to the IRS in 2023 will look like this (the version furnished to Dan will include truncated social security numbers):

Thank you for accessing Kinney Health Compliance.

You must own a Affordable Care Act Membership Plan to continue reading.

C. SSN or other TIN versus Date of Birth

Employers filing Forms 1095-B or 1095-C must report a Social Security Number (SSN) or other Tax Identification Number (TIN) [1] for every spouse and covered dependent. The instructions for these forms tell you to include a date of birth for the dependent only if the line for the SSN or TIN is left blank. But they don’t tell you how hard you have to try to get the social security number. When you ask your employees for the social security numbers of their spouses and children, many will respond that it’s none of your business, and they have a good point. The more you put that type of information out there, the more likely it is to be stolen.

With elimination of the “good faith” defense for incomplete or incorrect information in Forms 1094 and 1095, employers may be nervous about using dates of birth rather than SSNs or other TINs. But the regulations are not a model of clarity.

Thank you for accessing Kinney Health Compliance.

You must own a Affordable Care Act Membership Plan to continue reading.

D. Reporting Health Reimbursement Arrangements (including VEBA-HRAs) on Form 1094-B (Full-Text)

Health Reimbursement Arrangements (HRAs) and VEBA-HRAs are treated as providing minimum essential coverage (though they are noncompliant unless integrated with group health plan coverage. As a result, they are generally subject to reporting requirements under 1094 and 1095 B and C. Fortunately, there are several exceptions from the reporting requirement; and when reporting is required, an applicable large employer may use Form 1095-B rather than Form 1095-C.

D-1. Exceptions to reporting. An employer need not report coverage under an HRA or VEBA if any of the following apply:

- The employer maintains a self-insured major medical group health plan for which reporting is required, and the employee is enrolled in the health plan and an HRA or VEBA.

- The employer maintains a fully insured major medical group health plan for which reporting is required, and the employee is enrolled in the health plan and an HRA or VEBA.

- A former employee is enrolled in government-sponsored coverage for which reporting is required, such as Medicare, Medicaid (called “Medical Assistance” or “MA” in Minnesota) and Tricare, and the employee has a retiree HRA or VEBA.[1]

- Although not directly addressed in guidance, we don’t think that reporting is required for employees or former employees in any year in which an employee opts out of and waives future reimbursements from HRA or VEBA accounts.[2]

D-2. When must HRAs and VEBA accounts be reported on Forms 1095-B and C? HRAs and VEBA accounts must be reported on Form 1095-C when provided to an employee who is eligible for and enrolled in a major medical group health plan through a spouse’s employer.

Unless they permanently opt out of and waive future reimbursements from their HRA and VEBA accounts (at least until they reach age 65), reporting is required for former employees who have group health coverage through another employer, coverage in the individual market (including MNsure), or have no other coverage.

Thank you for accessing Kinney Health Compliance.

You must own a Affordable Care Act Membership Plan to continue reading.

D-1. Exceptions to reporting

Thank you for accessing Kinney Health Compliance.

You must own a Affordable Care Act Membership Plan to continue reading.

D-2. When must HRAs and VEBA accounts be reported on Forms 1095-B and C?

Thank you for accessing Kinney Health Compliance.

You must own a Affordable Care Act Membership Plan to continue reading.

D-3. What forms should employers use to report HRAs and VEBA accounts?

Thank you for accessing Kinney Health Compliance.

You must own a Affordable Care Act Membership Plan to continue reading.