A. Overview

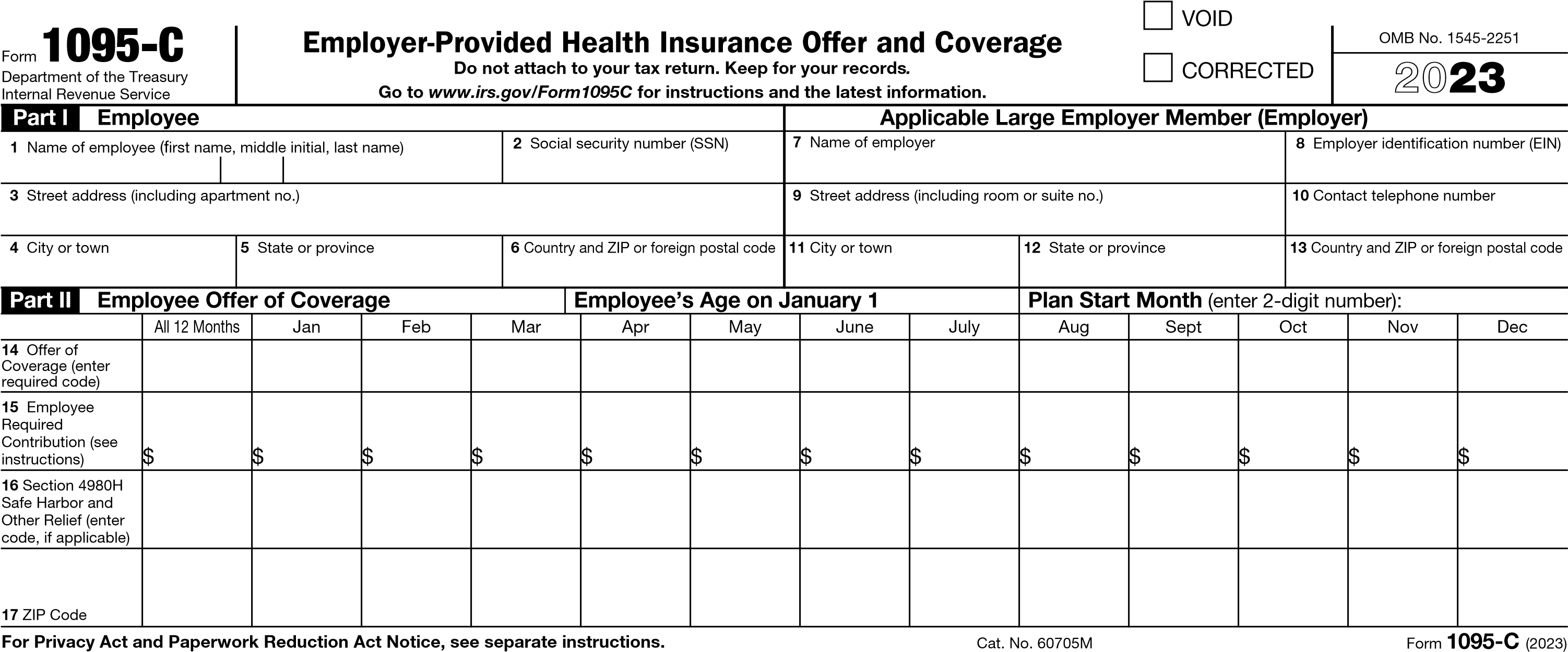

The beating heart of Form 1095-C for applicable large employers is found in lines 14 through 16 of Form 1095-C, reproduced below. Lines 14 and 16 on Form 1094-C require that you report “codes” for each employee enrolled in coverage for every month of the calendar year, and for every employee who was a full-time employee in every month of the calendar year. Various writers claim there are between 90 and 198 possible code combinations on those lines, though not being mathematicians, we won’t hazard a guess. Despite all those options, there are circumstances that do not seem to fit within any possible combination. We’ve heard of code combinations that trigger sirens and alarms at the IRS headquarters in Washington, DC. At least one combination, which we won’t mention here, may cause the Air Force to scramble fighter jets.

Line 15 requires that you share the amount that employees must pay for self-only coverage (even if they elect family coverage). Most Minnesota public employers use the Federal Poverty Line Safe Harbor, which we describe here. This amount varies depending on whether the employer is using a calendar plan year or a non-calendar plan year, and it can get a little weird for non-calendar plan years.

Here is how it looks empty – it reminds us of a football field.

Many employers have received Form 226J letters from the IRS (proposing penalties) because they used the wrong codes in error, making it appear that they were not offering affordable coverage to their full-time employees when in fact they were. In responding to Form 226J, employers have been able to avoid Employer Shared Responsibility penalties by acknowledging mistakes in reporting that were made in “good faith.” These same arguments will likely still work in the future to avoid penalties under 4980H(a) and (b), but another penalty is looming over the horizon.

B. Elimination of Good Faith Relief

When IRS information returns are incorrect, incomplete, or filed late, the IRS will assess penalties under Sections 6721 and 6722 of the Code. From 2015 to 2020, the IRS offered relief from these penalties for making mistakes on Forms 1094 and 1095, provided they were made in “good faith.” It’s pretty easy to make a good faith mistake in filling out form 1095-C.

In December of 2021, the IRS announced that the “good faith” defense for errors in Forms 1094 and 1095 will no longer be permitted, because they “have now been in place for six years, and transitional relief is no longer appropriate.”[1]

Thank you for accessing Kinney Health Compliance.

You must own a Affordable Care Act Membership Plan to continue reading.

C. Reporting Basics

Who Must File Forms 1095-C?

- Every “Applicable Large Employer” (with 50 or more full-time employees and full-time employee equivalents in the previous year) must furnish and file Form 1095-C for each employee who was a full-time employee in any month during previous year. This includes “ALE Members” – employers which themselves may not have 50 or more full-time employees and FTE equivalents, but that are under common control with a group of employers (an “Aggregated ALE Group”) which taken together have 50 or more full-time employees and FTE equivalents.[1] We discuss the controlled group rules

- Each ALE Member must file its own Forms 1094-C and 1095-C under its own separate Employer Identification Number (“EIN”), even if the ALE Member is part of an Aggregated ALE Group. No “Authoritative Transmittal” (line 19 of Form 1094-C) should be filed for an Aggregated ALE Group as a whole. Each ALE Member files their own Forms 1094-C and 1095-Cs, and each indicates that it is an Authoritative Transmittal on Form 1094-C. (Note that one ALE Member can’t blow it for the whole group. If a municipal liquor store has a separate EIN and board of directors, but the city appoints at least 80% of the board members — putting them under common control with the city – the liquor store will be an ALE member required to file Forms 1094-C and 1095-C even if they have just a handful of employees. If they screw up, the penalty will be localized and limited to the liquor store.)

- Form 1095-C must be furnished and filed for any employee who was a full-time employee during any month of the year. It must also be furnished and filed for part-time employees, if they are eligible for and enroll in coverage.

Thank you for accessing Kinney Health Compliance.

You must own a Affordable Care Act Membership Plan to continue reading.

D. Part I of Form 1094-C

Part I—Employee

Line 1. Enter the name of the employee (first name, middle initial, last name).

Line 2. Enter the 9-digit SSN of the employee (including the dashes).

Thank you for accessing Kinney Health Compliance.

You must own a Affordable Care Act Membership Plan to continue reading.

E. Part II of Form 1095-C: The Fun Begins (Full-Text)

The top of Form 1095-C, Part II reads as follows:

Part II | Employee Offer of Coverage | Employee’s Age on Jan 1: | Plan Start Month (2 digit no.): |

E-1. Top of Form. The “Employee’s Age on Jan 1” line only needs to be completed if you have an ICHRA (most will leave this blank). The “Plan Start Month” is required, and you have to complete that box by entering the 2-digit number (01 through 12) that corresponds with the first calendar month of the health plan year in which the employee is offered coverage (or would be offered coverage if the employee were eligible to participate in the plan). If more than one plan year could apply (for instance, if the ALE Member changes the plan year during the year), enter the earliest applicable month. If there is no health plan under which coverage is offered to the employee, enter “00.” You don’t have to file Form 1095-C for part-time employees or non-employees who are not offered coverage, so keep in mind that if you enter “00”, it means that you are filing Form 1095-C for a full-time employee who was not offered coverage. This could potentially result in penalties under Section 4980H(a) or (b).

E-2. Line 14: Code Series 1—Offer of Coverage. The Code Series 1 codes specify the type of coverage, if any, offered to an employee, the employee’s spouse, and the employee’s dependents. Keep in mind that codes in Lines 14, 15, and 6 are related to one another; put another way, what you report in Line 14 has a “ripple effect” through the rest of Part II. Buckle up!

Code 1A. Qualifying Offer: Minimum essential coverage [“MEC”] providing minimum value [“MV”] offered to full-time employee with Employee Required Contribution equal to or less than 9.5% (as adjusted) of mainland single federal poverty line and at least minimum essential coverage offered to spouse and dependent(s). This code may be used to report specific months for which a Qualifying Offer was made, even if the employee did not receive a Qualifying Offer for all 12 months of the calendar year.

Thank you for accessing Kinney Health Compliance.

You must own a Affordable Care Act Membership Plan to continue reading.

E-1. Top of Form

Thank you for accessing Kinney Health Compliance. You must own a Affordable Care Act Membership Plan to continue reading.

E-2. Line 14: Code Series 1—Offer of Coverage

The Code Series 1 codes specify the type of coverage, if any, offered to an employee, the employee’s spouse, and the employee’s dependents. Keep in mind that codes in Lines 14, 15, and 6 are related to one another; put another way, what you report in Line 14 has a “ripple effect” through the rest of Part II. Buckle up!

Code 1A. Qualifying Offer: Minimum essential coverage [“MEC”] providing minimum value [“MV”] offered to full-time employee with Employee Required Contribution equal to or less than 9.5% (as adjusted) of mainland single federal poverty line and at least minimum essential coverage offered to spouse and dependent(s). This code may be used to report specific months for which a Qualifying Offer was made, even if the employee did not receive a Qualifying Offer for all 12 months of the calendar year.

Comment: Almost all Minnesota public employers offer MEC that provides MV to their full-time employees, their spouses, and their dependents. The vast majority of public employers in Minnesota use the Federal Poverty Line Safe Harbor.

Code 1A is the gold standard and chances are you are already there. If you use this code in the “All 12 months” box for a full-time employee, you won’t have to complete Lines 15 and 16. If you use it for specific months, you won’t have to complete Lines 15 or 16 for those months. We like code 1A in line 14.

Thank you for accessing Kinney Health Compliance.

You must own a Affordable Care Act Membership Plan to continue reading.

F. Line 15: Employee Required Contributions

Line 15 is where you report the cost to the employee of the lowest cost self-only coverage, more commonly referred to as single coverage, even if the employee has elected a family coverage option. This reporting is required so the IRS can determine whether an offer of coverage is “affordable.” If an offer of coverage is not affordable, and a full-time employee obtains premium tax credits or cost reductions through MNsure, the employer will be penalized with the “bad” penalty under 4980H(b).

Depending on the code you use in line 14, you may leave line 15 blank. The instructions state that you should complete line 15 only if codes 1B, 1C, 1D, 1E, 1J, 1K, 1L, 1M, 1N, 1O, 1P, 1Q, 1T, or 1U are entered on line 14. That’s a lot of cross referencing, but let’s whittle down the list by taking out the ICHRA codes, since we’re not addressing them here. Absent the ICHRA codes, you have to complete line 15 if codes 1B, 1C, 1D, 1E, 1J, 1K are entered on line 14.

That makes it easier, but we still think it’s helpful to understand why line 15 should be completed or left blank. Let’s do a quick run through the codes in Line 14 and explain.

If the code you put in line 14 is. . .

Code 1A (Qualified Offer). Leave line 15 blank. Code 1A ticks all the boxes and conveys that you’re using the Federal Poverty Line Safe Harbor. You don’t have to complete line 16 either.

Thank you for accessing Kinney Health Compliance.

You must own a Affordable Care Act Membership Plan to continue reading.

G. Line 16: Code Series 2—Section 4980H Safe Harbor Codes and Other Relief for ALE Members

Line 16 is special. In some cases, no codes apply. In other cases, more than one code applies, and you’ll have to follow ordering rules to determine which code to enter. If the same code applies for all 12 calendar months, you may enter the code in the “All 12 Months” box and not complete the monthly boxes.

Line 16 is used to report that one of the following situations applies to employees:

- The employee was not employed or was not a full-time employee;

- The employee enrolled in the minimum essential coverage offered;

- The employee was in a Limited Non-Assessment Period (one of six types of waiting periods);

- The ALE Member met one of the Affordability Safe Harbors with respect to this employee; or

- The ALE Member was eligible for multiemployer interim rule relief for this employee. This means that the employer contributes to a multiemployer health plan (such as a Taft Hartley plan) to meet its obligations under the ACA. We’ll provide more background on multiemployer plans when we describe code 2E.

Thank you for accessing Kinney Health Compliance.

You must own a Affordable Care Act Membership Plan to continue reading.

H. Part III of Form 1095-C

- Only complete for employees (and spouses and dependents) who actually enroll in employer-sponsored coverage

- Enter the name, Social Security Number and Date of Birth (if the SSN is not available) for all covered individuals (participant, spouse and dependents)

Thank you for accessing Kinney Health Compliance.

You must own a Affordable Care Act Membership Plan to continue reading.